Most cards offer you a number of days where you will not be charged interest on your purchases (this doesn’t usually apply to cash advances or balance transfers). The number of interest-free days varies by credit card, and can be anywhere from 35 to 56 days, or more.

This concept can be very misleading though, because it doesn’t mean you get that number of days after each individual purchase.

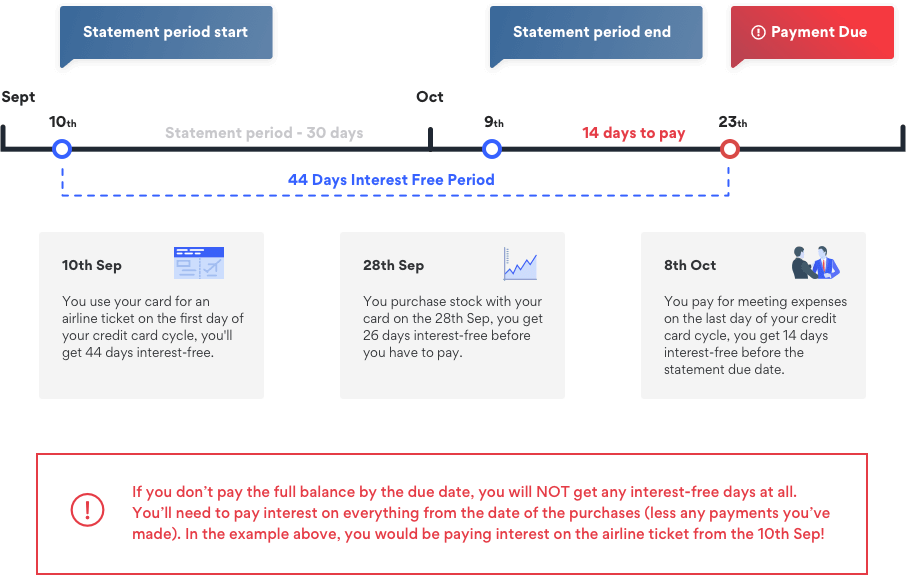

What actually happens is that each month you will receive a statement showing your total credit balance, and you’ll have a ‘grace’ period of, for example, 14 days from the date of the statement to pay it off in full.

The grace period (e.g. 14 days), plus the days in the billing cycle when you made the purchase (e.g. 30 days), together make up the interest-free period (e.g. 44 days). So, in this example, if you buy something on the last day before the end of your billing cycle, you’ll actually only get 15 interest-free days on that purchase.

It’s very important to note that the interest-free period only applies if you pay off the full balance shown on your statement by the end of the grace period. If you don’t, you’ll be charged interest on the unpaid balance from the date of each purchase, not from the end of the interest-free period.

When weighing up your options, the value of the interest-free period to your business will really depend on how you expect to use your card. Obviously, the more interest-free days you have, the longer you can have that cash at your disposal, which can be valuable if cashflow is tight.

But if you aren’t expecting to pay off your full credit card balance each month, interest-free days are likely to be much less important to you than a low interest rate on purchases.