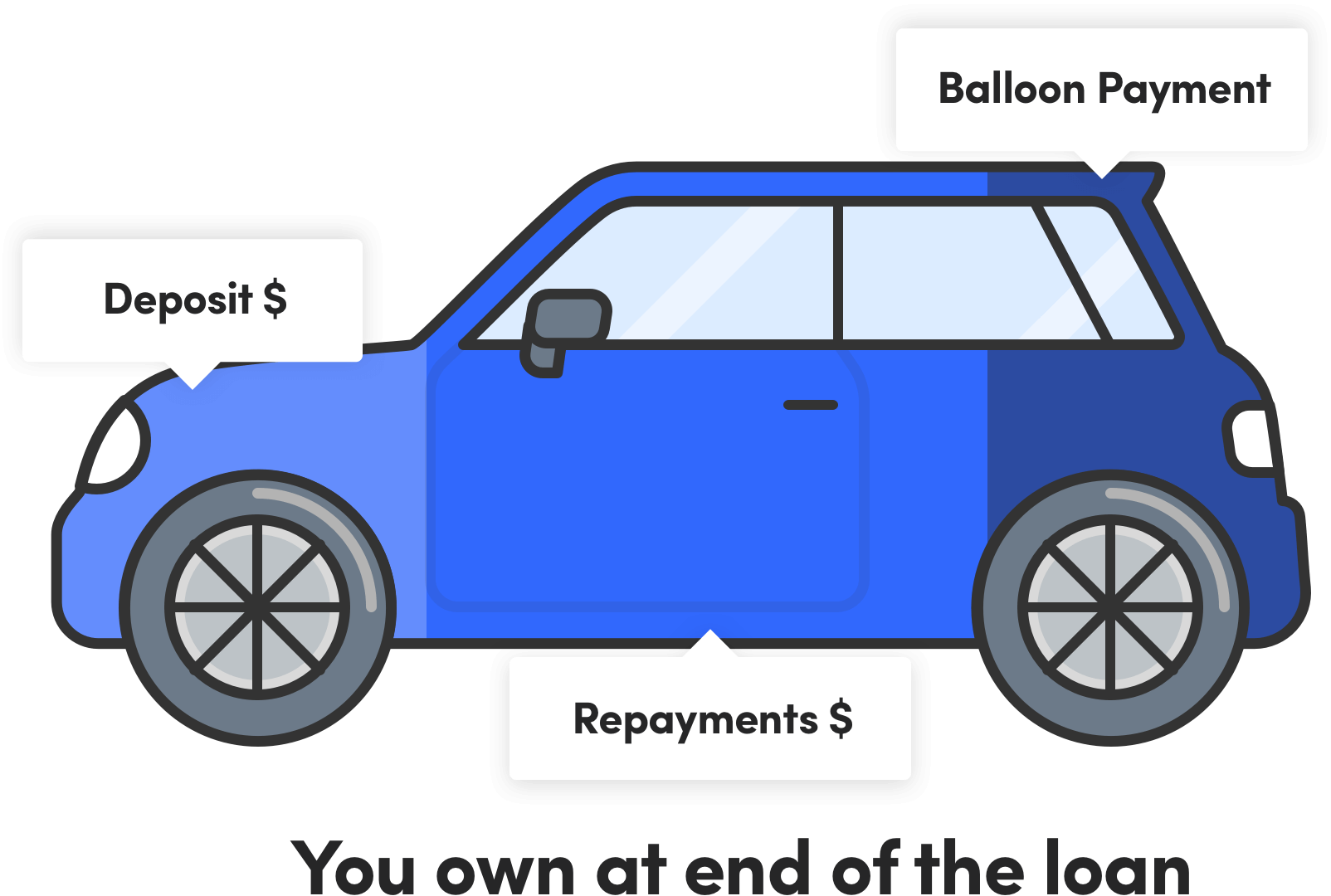

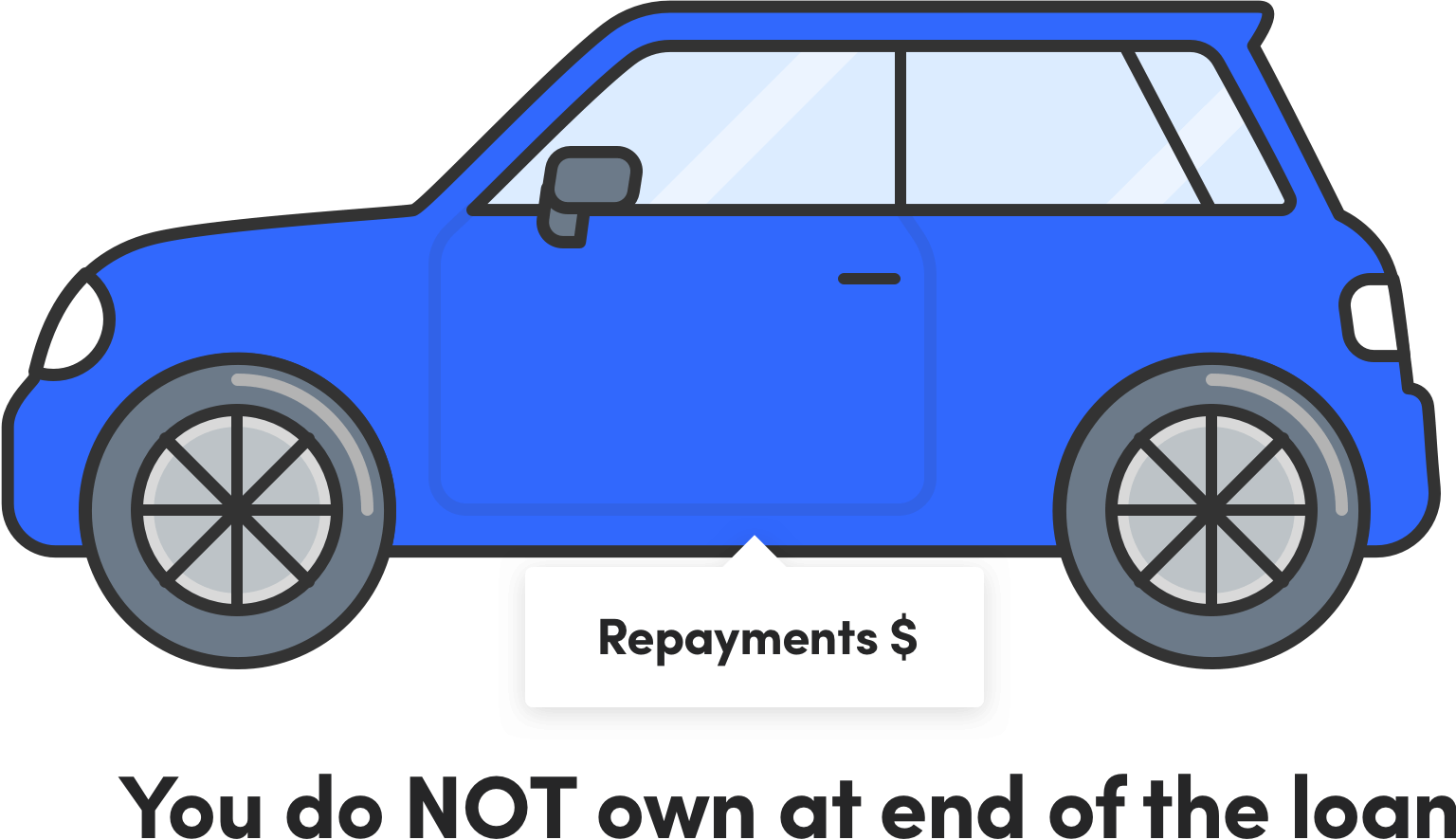

“When you’re buying vehicles in a business context it’s easy to focus narrowly on the tax implications of the various types of finance. And while it’s essential you make the right choices there, you need to realise there are real gains in considering on the fundamentals more broadly: Negotiating effectively the lowest price on the new vehicle(s) together with the highest prices for the vehicle(s) you are disposing of, together with the lowest cost of whatever finance scheme is appropriate to your business. There are a lot of moving parts in most vehicle upgrade transactions, and car dealers (plus other parties to these transactions) are very effective advocates for their own profit here. Your mission, somewhat in opposition, is to be a balancing influence, and become an effective advocate for your own best financial interests. You have to drive a hard bargain at every point.”